Retirement != Social Security Time

One of the biggest false constructs people have in their minds about social security is that they have to take it once they retire. I’m still not entirely sure if they think it is a literal requirement, or just an ironclad rule of good financial management, but it is overwhelmingly common.

Part of the problem probably lies with the most common language used around social security, “full retirement age”. Most people who turn 62 begin to educate themselves on their options, at least enough to know that every year they wait up till 70, they will increase their benefit (unless they are going to claim a spousal benefit, in which case they top out at 66 or 67 or some point in between).

For single people, especially healthy, wealthy ones (the kind that retire at 60 so they can travel Europe and hike while they have two good knees), it often makes sense financially to draw a little more from the portfolio from 62 until 70 for the enhanced benefit starting at age 70.

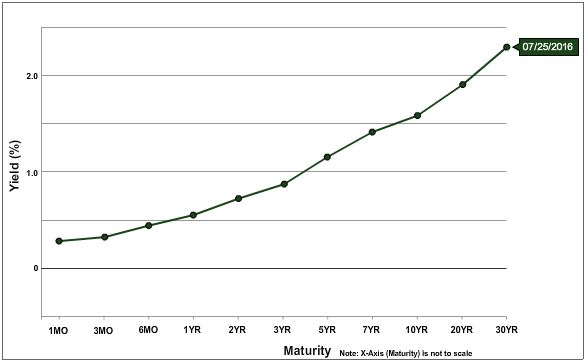

Why? Because the increase to social security is mostly risk free (some political risk, but the odds that two people of the same age won’t get grandfathered in because one started benefits and the other didn’t strikes me as tiny), and that increase is close to 8% (the math changes part-way through), which you would be wise to note, is much higher than that other risk-free return, treasuries.

Yes, that’s 2% at the top of the graph. And yes, it does feel different to have a social security benefit that is growing at 8% per year versus having a portfolio with a balance that you can see growing at 8%, but the math is pretty much the same, and math doesn’t care how you feel about it.

The other nice thing about social security is that it is a form of insurance (in fact, your benefit at full retirement age is known as your primary insurance amount (PIA). If you do the riskiest thing in finance (well, besides invest with this guy), live a long life, the returns on delaying social security just compound and compound. If you die early (e.g., 72), yes your decision to wait sucked, but it turns out you didn’t need that money anyway!

Now, obviously there are cases where someone has saved next to nothing for retirement and can’t continue to work past 62, and they will draw social security as soon as they can, but for people who don’t fit into that bucket, just remember, you don’t have to take social security when you retire, you can file for medicare separately, and you’ll probably be better off to wait.

Couples is a more complicated issue as far as when they should begin taking benefits, although it got simpler/more complicated with the elimination of file & suspend. I haven’t taken the time to flesh out my new preferred rules of thumb (RIP to my file & suspend spreadsheet, you were so beautiful), so I won’t conjecture. But couples have the same option as single people, waiting to take benefits, even if they consider themselves “retired”.

So please, old(er) folks, don’t feel pressured by your friends or colleagues or CNBC (do they talk about social security?) to begin your social security benefits the day you walk out the door from your retirement party.