Understanding the risk vs. return trade-off is something that takes people in finance entire careers. It is an always developing understanding.

To see some beautiful thoughts developed over some of those aforementioned careers, check out this post by Nassim Taleb and this one by Howard Marks.

Here I’m going to focus on much simpler definitions and relationships.

If you are to take a risk, you have to be rewarded for it. The more risk, the more reward you will demand. This is true for people and also for markets. This is the reason why companies and countries with good credit ratings can sell bonds that pay lower interest rates.

However, it’s important to remember that something that is riskier, won’t necessarily return more over any given time period. In fact, by definition, if it would, it would be less risky. The only return that is higher for riskier assets is the expected return.

In fact, a brief digression. A common example of this principal bleeding into the world is that something can be ‘too good to be true’. In investing, something that looks (or is claimed by a salesman) to be low risk, but promises high returns, is probably a sign that there is hidden risk somewhere.

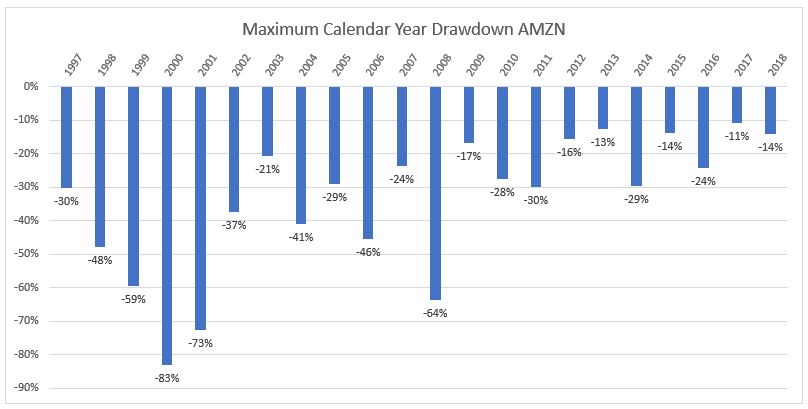

Using the same example as in my bond primer post, Tesla has both bonds and stock that you can purchase. If you buy the bonds, you expect a lower return, and also a lower variance in the potential outcomes of the investment. You may expect to get 7% return, and a bad outcome is that you lose 10% of your investment, while a good outcome is that you get 10%. In fact, with bonds, the best case outcome is almost always known and capped ahead of time. If you buy Tesla stock, you may expect to get 20% returns, but you may very well lose all of your money, or have returns much higher than 20%. This is risk.

As discussed in the purpose of investing, even if you can get higher returns, you may prefer a lower expected return and lower risk portfolio, especially if both will accomplish your goals equally well.